Content

Links and Resources (here you can find all links and sources mentioned in the article)

- Intro

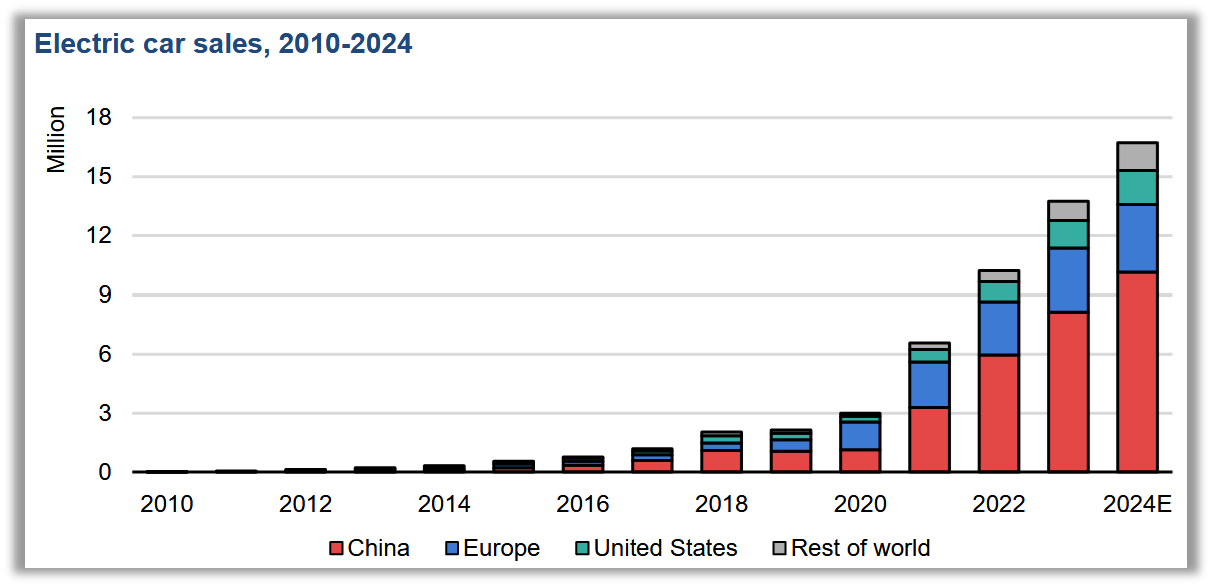

Today, there are 30 Mln fully electric vehicles on the market globally, which makes up less than 3% of the vehicle market. New electric vehicle sales are already more than 15%, but “EV growth speed bumps” are starting to appear.

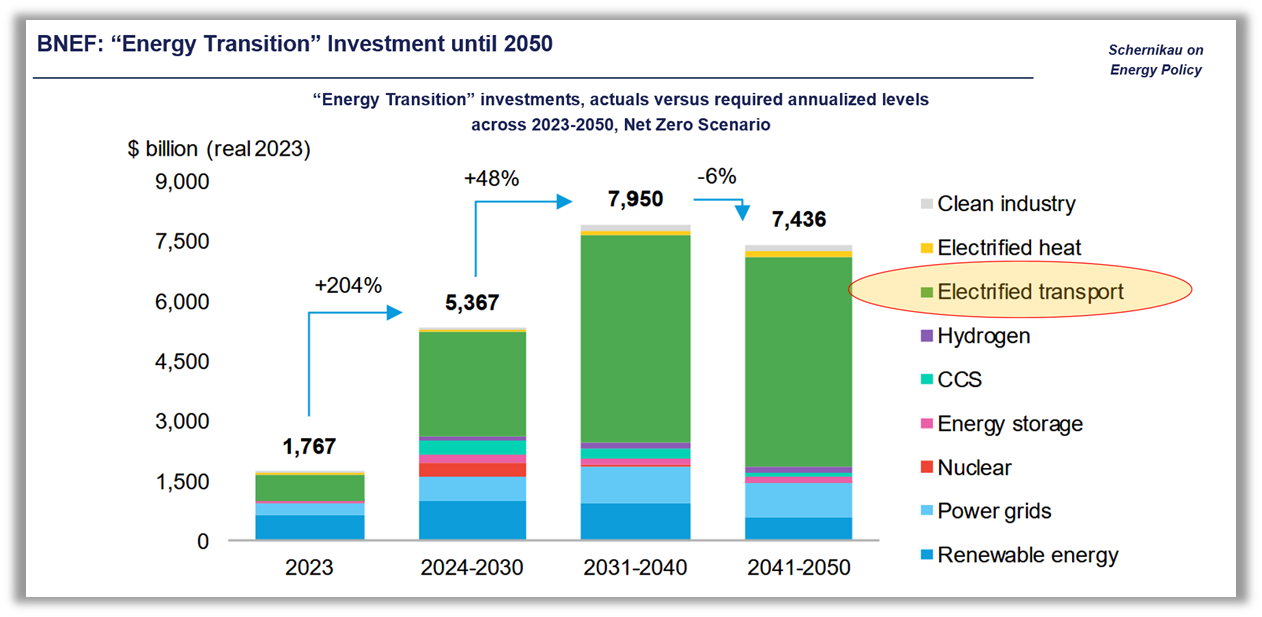

Did you know, “Electrified Transport” is the single biggest investment envisioned for achieving “NetZero”? In May 2024, Bloomberg New Energy Finance BNEF reported that we need to invest on average an annual $ 4.4 Tln, or cumulatively $ 120 Tln, in EVs from 2024 through to 2050, in order to reach “NetZero”! (Link in Links and Resources below) No wonder this is a “popular” industry to be in… definitely worth to explore how to get a piece of that pie, don’t you think?

Here I will not cover the incorrect “net zero” assumptions that BNEF and others make about EVs, which will be quite obvious to you once you reach the end of this article. As per BNEF “electrified transport”, already received $600 Bln investment in 2023 alone, so to reach goals, this number “only” needs to multiply 8x on average for the next two and half decades (Figure 1: Energy Transition Investments).

This is part 2 of a 2-part series, focusing on the supply chain of EVs and their impact on our power systems. Part 1 focused on the history of EVs and current market overview.

Electric motors always had a much wider use case than transportation. In fact, electric vehicles (EVs) appeared rather secondary. Electric motors were used for an array of industrial and consumer applications, but always requiring an external power source, connected by a wire (see modern trains). The idea to completely “electrify” transport comes from the wish to replace oil-based CO2 emitting fuels with “zero CO2 ” electricity to “save the environment” (which I assume “the climate” is part of).

Figure 1: Energy Transition Investments

Source: BNEF NEO 2024 Link in Links and Resources below)

Chinese manufacturers, in order of importance BYD, SAIC, Seres, Li-Auto, Chery, GAC Aion, Great Wall Auto, Zeekr, Nio and more, are taking over the market fast. They are growing while western auto manufacturers appear to be stumbling.

Although government subsidies and support for EVs, battery and charging infrastructure amount to billions, the sentiment in Europe and North America is changing, with subsidies slowly drying up. Germany’s slump in EV sales in the first half of 2024 is evidential of this. EV auto manufacturers around the globe are in trouble it seems.

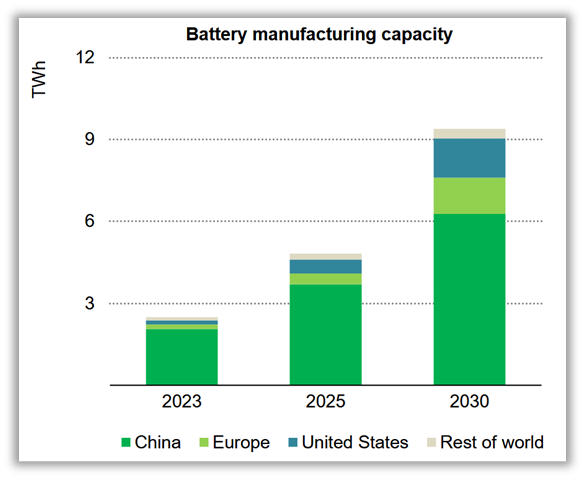

Taking a step back, let`s consider the conversion process within the vehicle (fuel to motion, vs electricity to motion) We can agree that EVs are much more efficient, but what happens before the conversion process, is largely about battery manufacturing. Battery “making” is expected to reach 9 TWh output annually within the next 6 years, or the equivalent output of 180 Tesla Gigafactories producing 50 GWh every year.

What does this really mean for the environment we are aiming to protect?

Let’s have a look

Figure 2: Battery manufacturing capacity

Source: IEA World Energy Investment 2024, p148, based on Benchmark and Bloomberg

(Link in Links and Resources below)

2. Raw material and energy input

The raw material efficiency of cars is a key environmental consideration. Humanity’s goal should be to become more material and energy efficient in all our endeavors. That, by the way, does not mean we will use less energy or raw materials, but rather aiming for higher efficiency, meaning we will be increasing utility thereof. Everything we produce and consume ultimately originates from “raw” materials, and so do electric and non-electric vehicles. So what is the problem then?

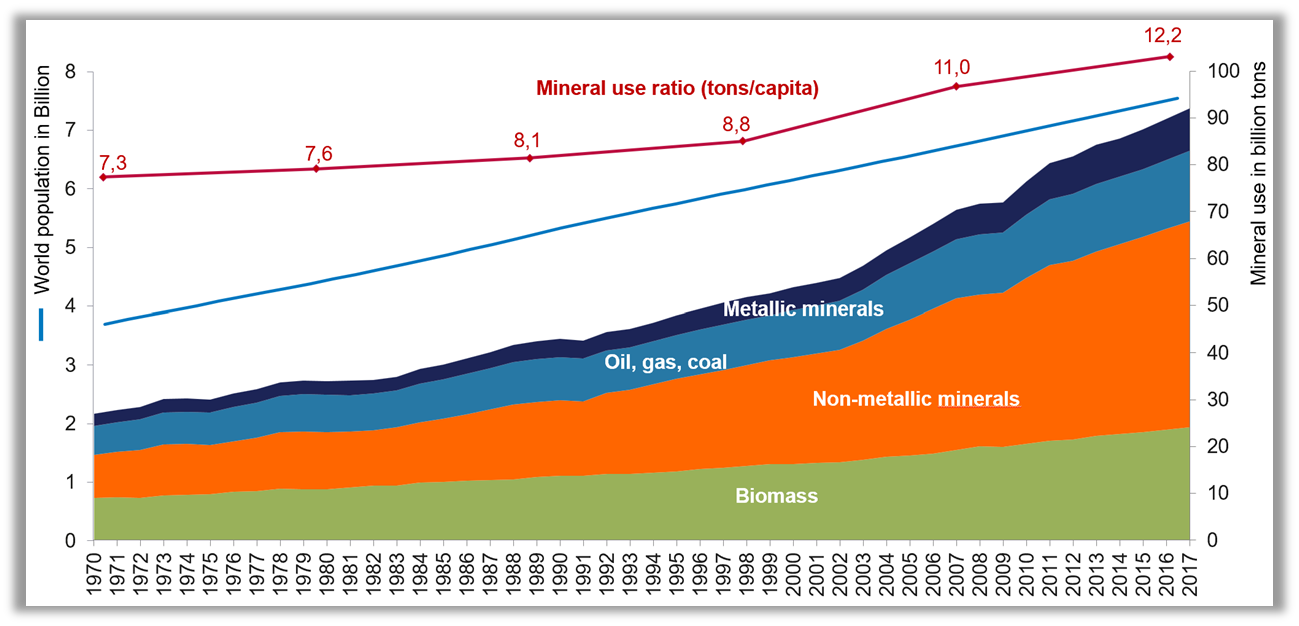

Figure 3 illustrates that for its existence, humanity today requires almost 100 Bln tons of grown and mined minerals. The material consumption per capita has been continuously increasing, which has been largely driven by the reduction of poverty. Classic fossil energy raw materials contributing to over 80% of global primary energy make up only ~15% of all minerals extracted.

When we speak of material input, we often consider steel, copper, cement, glass, aluminum, or silicon as base products as a direct input. However, as mentioned above, these materials must first be mined, produced and upgraded, requiring energy, from mined raw materials such as iron ore, coal, limestone, silicon, bauxite, quartz stone, etc.

Now getting back to EV batteries, which typically account for 30% to 40% of the value of an electric vehicles. Those batteries require input consisting of lots of non-metallic and metallic minerals… A 85 kWh battery for a Tesla, which is rather large and weighs about half a ton adjusting for the average ore grade (1-2%), requires about 25-50 tons of raw minerals to be mined, before the processing & transport chain can start. Is this considered as all green and “net-zero”? I have my justified doubts.

Figure 3: Global mineral extractions

Source: Schernikau/Smith Book, Chapter 2.6 “Unpopular Truth … about Electricity and the Future of Energy”,

Graph can be downloaded here

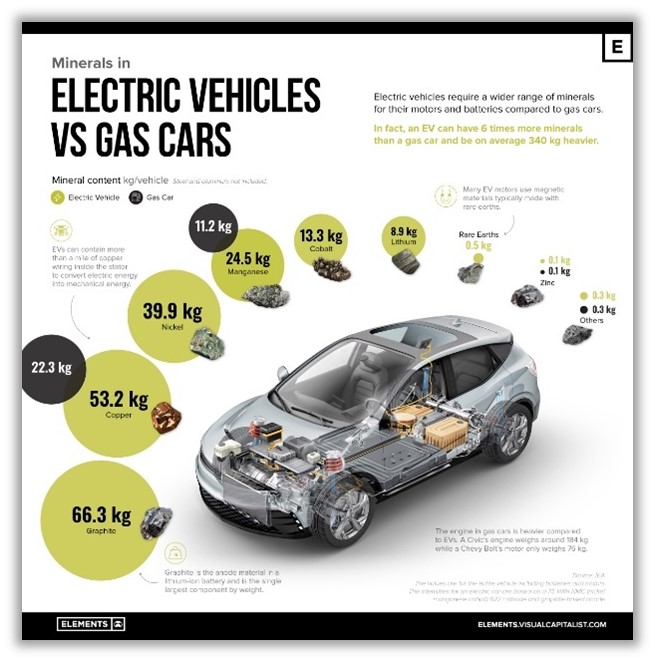

Figure 4: Demand for Battery Raw Materials

Source: Visual Capitalist 2023 based on Wood MacKenzie and IEA

(Link in Links and Resources below)

These minerals, depending on the battery type, usually make up the bulk of production (estimated in order of importance by Visual Capitalist 2022, Figure 4)

- Graphite

- Aluminum

- Nickel

- Copper

- Steel

- Manganese

- Cobalt

- Lithium

- And steel (iron)

The costs of a metal in both dollar and environmental terms are dictated primarily by ore grades, i.e., the share of the rock dug up that contains the metal sought. Also, related is the depth of the ore and thus the quantity of “overburden”—the rocks, dirt, trees, etc., on top of that the ore—that must first be removed.

Iron is a uniquely abundant metal in iron ore; not so the suite of critical “energy minerals,” for which ore grades range from 2% to 0.1%. Average nickel ore grade is under 2% and for copper below 1%, which means, arithmetically, that at least 1 ton of metal requires the discussed 25-50 tons of rock, excluding the overburden. Such geological realities determine the amount of energy used by big machines to do the digging, moving, grinding, transporting, refining, etc. (Mark Mills 2024, Link in Links and Resources below)

- assuming an 1:10 average overburden ratio, the tonnage to be moved would reach 250-500 tons for each Tesla Battery

In addition to the raw material tonnage you require significant amounts of energy in the form of heat and electricity for mining the materials and to manufacture the batteries. This energy is often called “embodied” energy of a product or material. For instance, aluminum has about 170,000 MJ per ton of embodied energy, while copper “only” has 60,000 MJ/t. I suspect these amounts do NOT truly include all energy required, but I speak under correction. The acclaimed book Sustainable Materials without the Hot Air by Cambridge researchers Allwood and Cullen 2015 summarizes the concept of embodied energy very well.

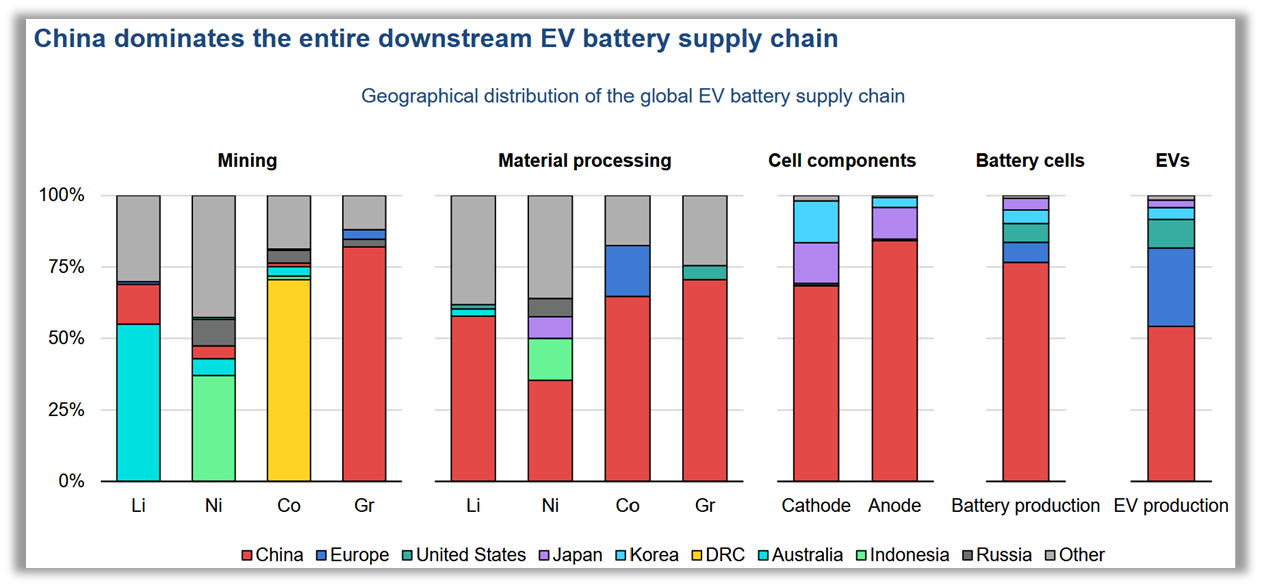

We understand that China dominates the entire value chain for batteries and most mineral processing (Figure 5), and we know how China provides the heat and electricity required for this process, which is largely with coal!

- Let us please also not forget that the chemical element carbon (from coal) is often required for chemical reduction (not just for heat or electricity). For instance, steel is an alloy of iron and carbon; it can also contain small quantities of silicon, phosphorus, sulfur, and oxygen.

- Each ton of steel requires ~1,6 tons of iron ore, ~800 kg of coal, and products such as limestone and various additives; let us approximate the total to ~2,5 tons of input raw materials for each ton of steel.

- Therefore, the ~2 billion tons of steel produced in 2022 required approximately 5 billion tons of raw materials which were extracted, transported, and processed. Thus, steel production appears to consume a little more than 5% of all global raw materials (from our book “The Unpopular Truth… about Electricity and the Future of Energy, Chapter 2.6).

- Oh, Silicon for solar panels also always require coal as a reductant.

Today, mining worldwide accounts for about 40% of global industrial energy use and over 10% of global final energy consumption. Diesel, or refined oil products, accounts for half of the mining-sector’s energy use. (Guilbaud 2016, Mark Mills 2023, Links in Links and Resources below)

Figure 5: China dominates EVs

Notes: Notes: Li = lithium; Ni = nickel; Co = cobalt; Gr = graphite; DRC = Democratic Republic of Congo

Sources: IEA 2022 based on Benchmark, US Geological Survey, BNEF, others

The fact that EVs are much more material intensive than standard vehicles is not disputed and has been confirmed by the IEA multiple times. I trust I don’t have to “prove” this here (Figure 4). Another logical point is that the larger the battery and bigger your vehicle (i.e. a bus or truck), or the longer the distance you travel, the more disadvantaged EVs are, when it comes to the raw material and energy “backpack” it carries, even before you turn it on the first time, in comparison to standard cars.

The idea is of course that once the car is built it emits “zero CO2 ” and makes up quickly for that “backpack”, which we will cover in the next section. The problem I see when equating CO2 efficiency with environmental protection, is covered in my article “The Dilemma of pricing CO2 ”.

Now, let’s ask who will produce all these raw materials? This is an interesting question with serious environmental consequences. The renowned energy economist Mark Mills 2024 pointed the following out “IEA says that will require hundreds of new mines. Benchmark Mineral Intelligence puts the number at 384 new mines just to meet EV needs for the graphite, lithium, nickel, and cobalt [that] will be required to meet EV demand by 2035.” (Link in Links and Resources below)

- Wood MacKenzie (Figure 4) estimated production increase of 6 “critical minerals” based on a much lower battery demand case of 8 TWh by 2050 than the IEA in Figure 2 with over 8 TWh by 2030…

- Prof Simon Michaux (Michaux 2024) has done advanced calculations with more realistic assumptions calculating that a largely electric vehicle fleet would require over 60 TWh of battery capacity for just “one generation”, as these batteries don’t last long.

- Schernikau/Smith 2021 calculated a theoretical solar-only powered Germany would require 2,25 TWh of batteries every single year (45 TWh total) for 14-day storage only, translating to over 5x global lithium production and over 20x global graphite anode production.

It seems like recycling and the “green circular economy” remain a distant dream. The IEA positively estimates that 1-2% of battery demand could come from “recycled minerals” (IEA 2022, Mark Mills 2023). But since batteries are, unrealistically, expected to last 10 years on average, recycling cannot play any significant role until mid 2030

To date, the “circular economy” consists of: (1) mining in Africa, (2) processing and manufacturing in China, (3) shipping to Europe and North America for a few years of usage, then (4) shipping the waste back to Africa for landfills. I have seen some of those landfills filled with European electronic waste in Africa with my own eyes (see also Deutsche Welle 2022, link in Links and Resources below)

In summary, evaluating the raw material requirements for the “EV Revolution” is such a tremendous task that only a few have truly mastered it. The IEA touches on some of those challenges in their reports but continuously underestimates the task. By the way, did you know the European Union classifies Coking Coal as a “critical mineral”, yet has stopped support for ALL coal projects in Poland and worldwide?

A recent IEA Tweet from Apr 2023 reads: “The scaling up of clean energy technologies will drive huge demand for the minerals & metals used to produce them.” Another IEA Tweet 2024 correctly states “The clean energy system requires more mineral resources than an energy system based on fossil fuels”.

If you want to better understand the challenges faced because of the raw materials required for the “EV revolution” you may also want to look at Mark Mills 2024 and watch his highly recommended and celebrated 45min video “The energy transition delusion: inescapable mineral realities” (Link in Links and Resources below)

I also recommend listening to or reading Prof Simon Michaux’s work (Michaux 2024). In his presented at the European Union he estimated that, if Europe was going 30% “non-fossil” by 2023, it would need 80 Mln EVs with 11 TWh of batteries and a few other things. If one assumes a 28-day buffer, Europe alone, by 2030 (6 years) will require 280 years of current annual production of lithium.

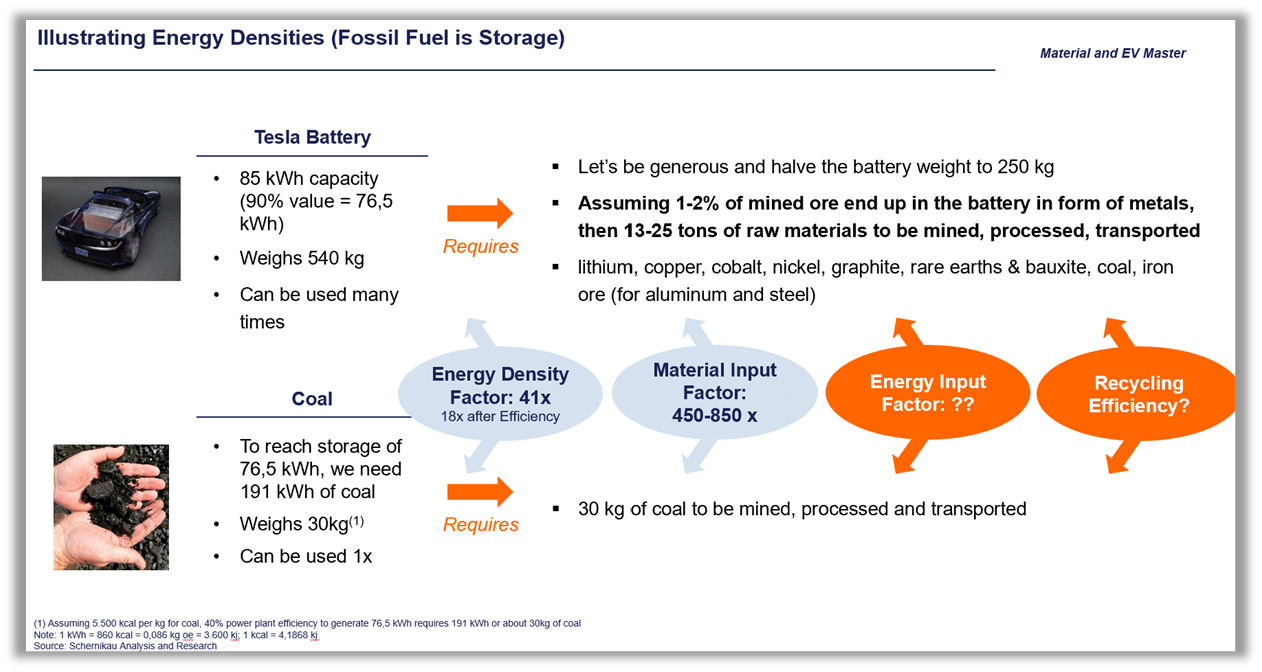

Figure 6: Energy density of batteries and coal

Source: Schernikau/Smith Book, Chapter 2.6 “Unpopular Truth … about Electricity and the Future of Energy”,

Graph can be downloaded here

3. Sources of power

We now understand what it takes to “just” build batteries. However, remember that those batteries are not yet charged for use. Because of their low energy density (kWh per kg), they require a lot of upfront investments in the form of raw materials and energy and these “heavy energy storage units” need to be carried around all the time (Figure 6: Energy density of batteries and coal).

How will we charge these batteries? The electricity required for charging will come from the grid. If you are very affluent, have your own power source (solar?) and storage to get through days or weeks of no sun or wind (batteries and hydrogen?) you could potentially be independent and completely off the grid. But I have yet to see a small town in Europe or the US that is truly off the grid.

Only if you had to truly and entirely be disconnected from the grid at all times, would the utility NOT have to consider your EV’s power demand. The fact remains that on average you will depend on the grid as the source of power or at least a backup for the worst-case scenario. My own analysis illustrates that every single month there is practically no wind and solar in Germany during the worst 4h periods (Figure 7).

That EV’s can be charged from your rooftop solar panels is a novel idea and may be possible during sunshine hours. But thinking your EV battery can act as storage for “dark” hours means you can’t drive the day after it was “dark”. And of course, the idea of using EV batteries as grid storage is a completely unrealistic notion.

Figure 7: Worst 4h Wind and Solar period each month in Germany

Sources: Schernikau, based on Agora actual data

How much power do large amounts of EVs need?

How much power would you then require? Let’s revert to a theoretical case – if 60 Mln German vehicles were all electric, each running on a 60 kWh battery

The short answer: peak power demand in Germany would double from 80+ GW to 160+ GW

The slightly longer answer would be – if we wanted to charge all 60 Mln cars throughout the year, considering wintertime with very little solar power potential and sometimes very little wind for extended periods. Here five assumptions:

- Weekly charge required is 40 kWh (about 200km per week, or 10.000km p.a.), about 125 TWh p.a. (40k Wh x 60 Mln x 52 weeks)

- Battery weighs 5 kg per 1 kWh (500kg for a Tesla 100 kWh battery)

- Average 2% ore metal ratio in batteries… meaning average copper ore, lithium ore, nickel ore, bauxite ore, cobalt ore, etc… 2% content in mined ore (of course it varies very widely from 0,05 to may be 20%)

- Average charger used 50 kW (Tesla’s fast chargers reach 100 kW or even 250 kW, see V3 and V4

- One Tesla Gigafactory manages to produce 50 GWh batteries p.a. (Tesla Berlin has plans to double to 100 GWh)

For the calculation, the charging pattern is key: One week has 168 hours, so on average 357.000 cars per hour (60 Mln / 168h) to be exact a 40 kWh charge takes 48 min with a 50 kW charger.

- 60 Mln cars with 60 kWh batteries = 3,6 TWh battery capacity in total, to be replaced every 10 years, thus 360 GWh new batteries each year

- That means it would take 72 Gigafactories 1 year to produce this or 7 factories would work constantly, all year-round to produce batteries continuously for Germany alone

- Batteries would weigh 18 Mln tons

- About 1 Bln tons raw materials would have to be mined, transported, processed, upgraded, etc, or about 100 Mln tons each year if the cars are replaced every 10 years (with no growth and negligible recycling)

- at an overburden ratio of 10:1 this would mean 10 Bln tons of overburden to move to get to the ore

- 40 kWh charge per week if spaced perfectly, would mean 357.000 cars charge with a 50 kW charger = 18 GW peak power…

- But more realistically perfectly spaced is impossible, and assuming only 5x inefficiency, then 1,8 Mln cars (which equates to 3% of the fleet) could charge at same time translating to about 90 GW peak power demand… and the grid has to be ready for that.

In the most positive scenario, it would mean that Germany’s peak power demand would double from currently 80+ GW to 160+ GW. Remember that wind and solar are NOT peak power capable without effective energy storage… only coal, gas, hydro, biomass and nuclear are. Also remember that we have NOT yet considered the electricity demand of those 7 Gigafactories running around the clock, nor the charging infrastructure, power lines and more… all requiring energy and raw materials, that still need to be built.

The increasing power demand from EVs was summarized by Bloomberg 2023 “Electric Vehicle Boom May Force China to Burn More Dirty Coal”. (Link in Links and Resources below) There is no doubt that EVs already increase peak power and total power use everywhere in the world! But what does that mean for the grid mix, why is Bloomberg saying this about coal?

Here is an important point made by various energy economists respectively: it can be assumed that the additional power required for EVs (or AI) will be less “green” than the average power in the grid. Follow this logic …and let me know if I am mistaken.

- We are already doing everything possible to install as much wind and solar, with or without additional EVs. We should assume we cannot do more. The average grid power over a year thus has X% wind and solar (in Germany about 40% in 2023, after 33% in 2022), and a small fraction of curtailed unused wind and solar Y%.

- Additional demand from1 Mln EVs (approx. 1,3 GW peak power, 2 TWh p.a.) will now have to come from somewhere… and that being a) curtailed wind and solar or b) from none-wind and solar, conventional power supply, also at times and wind and solar contribute practically zero (Figure 7).

- If (1) and (2) are correct, and Y% is far less than X, then logically the additional demand from EVs will reduce the average % of wind and solar in the system and increase “emissions”.

- Koch and Boehle 2021 wrote a peer-reviewed paper on this subject (Link in Links and Resources below)

That a larger power system also has other implications for the environment and the total cost of the power system should be clear by now. More trees for utility-poles (see Wallstreet Journal article “The Electric-Car Era Needs a Lot of Really Big Trees”, WSJ 2023), additional “power plants”, more complex distribution systems, disposal and waste issues, just to name a few.

Germany’s investment of over $6 billion in EV charging infrastructure shows a crucial step towards accommodating the electric vehicle influx, but does this make environment and economical sense? Who is footing the bill and where will the raw materials and energy come from to build these chargers? What is the “asset utilization”, who maintains them where are the chargers disposed of after their useful life? On and on the questions go. We understand that even the most pro-active scenarios mean that ICE and EV will live side by side for many decades, leading to duplication of infrastructure (existing gas stations and new charging infrastructure).

- The fact is that charging stations are, economically much more problematic. You fuel your car in 5 minutes but to charge an EV fully can take hours (depending on the charging power) thus, reducing serviced customers per day, leading to a need for a multiple of charging stations to “replace” the utility of one single nozzle at a gas station.

When it comes to charging, the issues are (1) where and how the electricity is produced and (2) how the electricity gets to the electric engines. Today’s trains run on rail with overhead connections to the powerplant (usually coal, gas, or nuclear) that is overall quite efficient. An EV on the road however, is supposed to use only “green” electricity from wind, solar and hydrogen and then use a battery to store this energy for future use? I hope you see why this is an unrealistic hope.

For that reason, EVs are not truly as “green” as they are usually portrayed. I would like to reiterate, that I am in support of electric vehicles where the consumer choses and where it makes a difference to divert emissions from city centres to rural areas globally. I simply question the global environmental and economic logic of forcing users from combustion to electric vehicles, not even touching on the “climate benefit”.

4. Safety concerns

There are three main risks to consider with a larger adoption of electric cars: 1) increased risk from heavier cars 2) increased explosion risk of batteries 3) significant performance decrease in high or low temperatures, i.e. when it snows, it increases safety risks.

The safety of current battery technology is a serious concern illustrated by a Chinese man (in July 2024) who carried his portable e-bike battery into an elevator, which subsequently lead to a deadly explosion in the closed elevator (see short not-kid-friendly video “eBike China 2024” under references). While this is an unusual and tragic event, it illustrates the seriousness of the explosion hazard posed. (Link in Links and Resources below)

We all hope the issue will be solved in the years and decades to come, but right now it remains a grave problem.

The list of issues with batteries is long. Travelling in Vietnam recently, I spoke to many a scooter drivers who told me anecdotes of how e-scooter users are switching back to fuel-based scooters simply because of so many examples of bikes igniting and exploding in homes. In Vietnam it is not unusual to park your motorbike in your living room overnight. We are all aware of how difficult it is to extinguish battery fires, hence airlines not allowing even a small 5.000 mAH battery pack to be carried in your check-in luggage.

Did you ever wonder why?

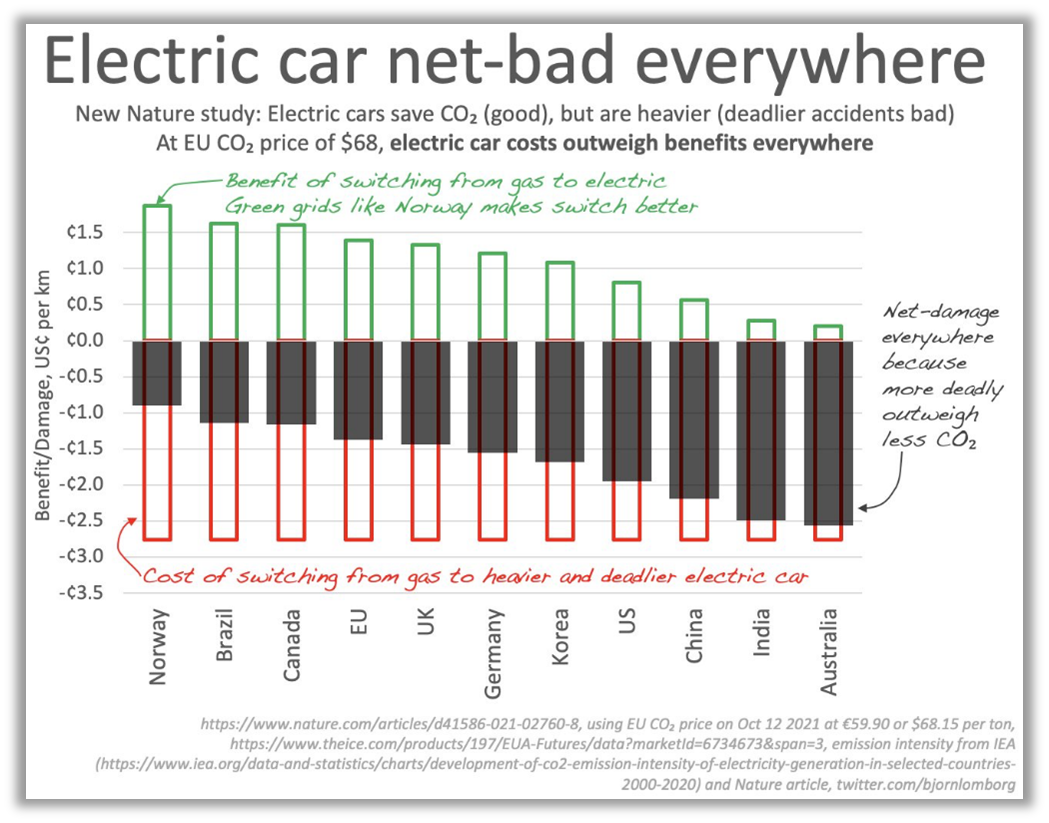

Battery powered cars are also deadlier because of their weight, a simple fact of life. Heavier, vehicles, by the way, has been proven to cause more particle pollution from tire abrasion. Dr. Bjorn Lomborg has summarized the trade-off in a simple graph. However, he was also not able to consider the true environmental impact of EVs, leading to positively exaggerated numbers (Figure 8).

Figure 8: electric cars are “net-bad” everywhere

A cherry-picked incomplete list of global responses to safety risk from batteries:

- National Transport Safety Board: Safety Risks to Emergency Responders from Lithium-Ion Battery Fires in Electric Vehicles (NTSB 2020)

- Insurer stops insuring EVs: John Lewis Stops Insuring Electric Cars over Repair Cost Fears (JohnLewis 2023)

- Extreme fire risk with EV´s exposed to salt water – Coast Guard issues alert to not allow on ships; CTIF – International Association of Fire Services for Safer Citizens through Skilled Firefighters (CTIF 2022)

- Germany, first city closes parking houses for EVs because of fire risk (Focus 2021)

It appears that electric car will NOT catch fire more frequently than standard cars (adjusted for driven km), but the severity of a fire is significantly worse, basically battery fires can hardly be extinguished. Countless stories globally illustrate this point. A simple google search will reveal more.

- eBike combusted in elevator in China, kills man, July 2024, (eBike China 2024)

- Tesla top-of-range car caught fire while owner was driving, lawyer says (Reuters 2021, Figure 9)

- A Lithium-Ion Battery Fire in a Cargo Ship’s Hold Is out after Several Days of Burning, Jan 2024 (AP News 2024)

- Massive Tesla Battery on Fire at Renewable Energy Plant in Australia, Jul 2021 (CNET 2021)

Figure 9: Tesla car caught fire while owner was driving

Source: Science Magazine 2021, Photo Wolfgang Rattay/Reuters

There are also risks associated with dead batteries leading to vehicles not being responsive

- Woman trapped in Tesla after Battery died (KKTV 2024)

- Numerous Tesla owners report being trapped (Yahoo 2024)

- Chicago shows Teslas struggle in cold weather. Here’s why (Quartz 2024)

Battery Dies in Cold Weather: Why? Renogy 2024 explains why battery cells are sensitive to environmental conditions. When the temperature drops significantly, it can cause serious damage to your batteries. But why do batteries die in the cold? When the temperature drops, the chemical reactions required to generate energy become slower and less efficient. This prolonged stress causes a degradation in capacity and discharge rate of the battery. Additionally, the battery becomes less mechanically stable, increasing the possibility of a sudden failure. Unfortunately, any temperature lower than 0 °C can cause appreciable damage to the batteries.

There is no surprise that Tesla had to “hide” battery issues and complaints for years (Reuters 2023), and that its range on average is far lower than stated.

The disposal of batteries is not discussed in more detail. But Science Magazine 2021 had a good short article “Millions of electric cars are coming. What happens to all the dead batteries?”. You can imagine the conclusion “Recycling researchers, meanwhile, say effective battery recycling will require more than just technological advances. The high cost of transporting combustible items long distances or across borders can discourage recycling”. In the meantime, we just dump those highly toxic batteries in Africa.

6. Summary

Again, I fully agree that there is a market for electric vehicles for instance in dense city centers, fixed routine work or the golf course.

- Yes, the electric engine, in itself, is more energy efficient than the internal combustion engine, but I strongly feel that we need to consider the entire supply chain from production to charging requirements, consumption, and then disposing of these toxic materials.

- The poor resale value and short lifespan of an EV, driven by the fast deterioration of the valuable battery, just creates another serious situation for the consumer to consider when it comes to buying an EV (TKP 2023).

- Even if, low energy dense batteries, were to double in energy efficiency, the peak power demand requirements make the widespread use of EVs in larger populated countries, completely unrealistic. It is, from an economical view, laughable to consider electric trucks, planes, and boats!

I vehemently protest government intervention in the choice for EVs vs ICE which largely has do to with the many environmental and economic issues which arise with a wider adoption of electric cars. For instance, a CO2 taxation of zero for EVs is as “ludicrous”, as the speed of a Tesla. The misinformation (nicely put) must be exposed, as only by shedding light on the situation and creating understanding, we will bring about positive change.

These proposed solutions merely divert emissions to other areas. We should be measuring all the safety hazards and also considering the total environmental and economic impact, which is clearly not positive at global scale.

There is so much still to be done, including a true-life cycle analysis of EVs and ICE at a scale that includes the entire supply and value chain from production to disposal.

Links and Resources

Here we show all references roughly in order of appearance in the article

- BNEF NEO 2024, New Energy Outlook 2024, BloombergNEF, May 2024, https://about.bnef.com/new-energy-outlook/

- IEA World Energy Investment 2024, p148, based on Benchmark and Bloomberg https://www.iea.org/reports/world-energy-investment-2024/overview-and-key-findings

- Mark Mills 2024, Electric Vehicles for Everyone? The Impossible Dream,” July 2023 https://manhattan.institute/article/electric-vehicles-for-everyone-the-impossible-dream/

- Visual Capitalist 2023, Visualizing Demand for Battery Raw Materials, Dec 2023, https://elements.visualcapitalist.com/visualizing-the-demand-for-battery-raw-materials/

- Visual Capitalist 2022, https://elements.visualcapitalist.com/the-key-minerals-in-an-ev-battery/

- Guilbaud 2016, PhD Thesis, University College London, https://discovery.ucl.ac.uk/id/eprint/1528681/1/FINAL%20PhDThesis_Joel_Guilbaud.pdf

- Bloomberg 2023: Electric Vehicle Boom May Force China to Burn More Dirty Coal,” April 2023. https://www.energyconnects.com/news/renewables/2023/april/electric-vehicle-boom-may-force-china-to-burn-more-dirty-coal/

- IEA 2022: Global Supply Chains of EV Batteries, July 2022, https://www.iea.org/reports/global-supply-chains-of-ev-batteries

- Deutsche Welle 2022: Activists slam Europe for dumping on Africa, https://www.dw.com/en/activists-slam-europe-for-dumping-on-africa/a-61315412

- Bloomberg, Jun 2022 https://www.bloomberg.com/news/articles/2022-06-01/will-electric-cars-take-over-they-must-sell-faster-to-reach-net-zero?utm_source=sendinblue&utm_campaign=2023-05-20%20Energy%20EV%20Special&utm_medium=email

- IEA EV Outlook, Apr 2024, https://www.iea.org/reports/global-ev-outlook-2024

- Michaux 2024, Prof Simon Micheaux, GFK, on youtube various videos, most recent one https://youtu.be/t6d7amHIXLg?feature=shared, more videos are here https://www.youtube.com/results?search_query=simon+michaux

- Mark Mills 2024, The energy transition delusion: inescapable mineral realities”, https://youtu.be/sgOEGKDVvsg

- BCG 2024: The Hidden Dynamics of the Green Transition” Jan 2024 https://www.bcg.com/publications/2024/the-hidden-dynamics-of-the-green-transition?utm_campaign=AI%20and%20Digital%20Transformation&utm_content=202401&utm_description=featured_insights&utm_geo=global&utm_medium=email&utm_source=esp&utm_topic=davos_2024&utm_usertoken=

- Bloomberg 2023: Electric Vehicle Boom May Force China to Burn More Dirty Coal, April 2023 https://www.energyconnects.com/news/renewables/2023/april/electric-vehicle-boom-may-force-china-to-burn-more-dirty-coal/

- Guilbaud 2016, University College London, PhD Thesis: Hybrid Renewable Power Systems for the Mining Industry, https://discovery.ucl.ac.uk/id/eprint/1528681/1/FINAL%20PhDThesis_Joel_Guilbaud.pdf

- Koch and Böhlke 2021, EVs-The Averaging Bias – a Standard Miscalculation, Which Extensively Underestimates Real CO2 Emissions, https://onlinelibrary.wiley.com/doi/full/10.1002/zamm.202100205

- WSJ 2023 Journal, Wall Street Journal. The Electric-Car Era Needs a Lot of Really Big Trees.” Nov 2023. https://www.wsj.com/business/the-electric-car-era-needs-a-lot-of-really-big-trees-e2b7ee92

- eBike China 2024, eBike combusted in elevator in China, Jul 2024 video, https://x.com/jenniferzeng97/status/1816126106627629217

- Renogy 2023, Battery Dies in Cold Weather: What Low Temperatures Do to Your Battery, May 2023, https://www.renogy.com/blog/battery-dies-in-cold-weather-what-low-temperatures-do-to-your-battery-/

- Reuters 2023, Tesla created secret team to suppress thousands of driving range complaints, Jul 2023, https://www.reuters.com/investigates/special-report/tesla-batteries-range/

- TKP 2023, Autohändler werfen das Handtuch bei E-Autos, tkp.at, Dec 2023. https://tkp.at/2023/12/28/autohaendler-werfen-das-handtuch-bei-e-autos/

IEA Outlook, April 2024