Content

- Intro

- EV a short history

- The current EV market

- Car companies, EV and not-EV

- CO2 footprint of EVs versus combustion engines?

- Summary

Links and Resources (here you can find all links and sources mentioned in the article)

Links and Resources (here you can find all links and sources mentioned in the article)

Globally, the EV narrative is gaining momentum, with over 16 million EVs, including hybrids, expected to roll off production lines in 2024 alone. This represents almost 20% of global car sales. Yet, these figures represent just a minority of the total global vehicle fleet of almost 1.5 billion (Figure 1: Global vehicle fleet), highlighting that we are only at the start of this “revolution” …or are we?

The electric motor is amazing. Its “invention” in the early parts of the 19th century involved Faraday, Jedlik, and many more. Also Orsted, Ampere, Maxwel, Herz, Tesla, Westinghouse and so many other famous names, with companies still carrying their names, are instrumental to today’s understanding of electricity and the motors or engines they power.

Following the first law of thermodynamics and electromagnetism, an electric motor “simply” converts electrical energy into mechanical energy. Btw, a generator in a power plant is principally an electric motor working the other way around, converting mechanical energy into electrical energy.

The development of the internal combustion engine (ICE) using oil-based liquid fuels took place more or less in parallel and took off in the 2nd half of the 19th century with inventors such as Nicolaus Otto, Gottlieb Daimler, Wilhelm Maybach, Karl Benz, Rudolf Diesel, and many more. The application of combustions engines went of course far beyond transportation but seemed to always be focused on making “driving machines”. This was the case because of the versatility and easy transportability of the liquid hydrocarbon fuel (petrol or diesel) they used.

Electric motors always had a much wider use case than transportation. In fact, electric vehicles (EVs) appeared rather secondary. Electric motors were used for an array of industrial and consumer applications, but always requiring an external power source, connected by a wire (see modern trains). For “wireless” transportation electric motors always required (1) sufficient electricity and (2) a battery to “carry” the electric energy.

When it comes to transportation, the principal difference between EVs vs internal combustion engine vehicles (ICE) appears obvious:

Let’s consider that liquid fuels and electricity are “free” as an “input” for both the Electric and ICE vehicles, it is then important to note that in transforming the input energy into mechanical forward motion, an electric engine is up to three times more “efficient” than a combustion engine (Sciendo 2020). This has to do with the thermal energy “lost” in the combustion process. There is a reason why today’s trains run on electricity and not on diesel anymore.

This apparent “conversion efficiency” also appears to be the basis for today’s push for EVs, coupled with the hope of practically unlimited “clean” electricity from wind and solar… what could be more obvious than to switch from combustion vehicles to electric vehicles? Well, let’s have a look… as always, in regards to energy, things are rarely simple and easy.

This is Part 1 in the 2-part series which focuses on the history and market overview of EVs. Part 2 will focus on EV’s impact on power systems and raw material supply chains plus explore the future.

By the way, I have to admit that I am not covering, but not forgetting, the important contribution of the steam engine. The steam engine is worth a whole chapter on its own, but since the steam engine is currently not “competing” with EVs, it is not covered here.

Figure 1: Global vehicle fleet forecast until 2040 – Bloomberg, June 2022

2. EV a short history

One hundred years ago electric cars were a common sight on city streets of Europe and the United States. Many of them had a range comparable to that of today’s EV’s.

Early EV manufacturers and battery makers could not agree on how to position the electric vehicle in the market. Some were convinced that “the electric” should be marketed as a short distance city vehicle. They saw it as a mistake to try and sell electric cars as a touring vehicle, because its range would always be inferior to that of a gasoline powered car.

Instead (like today), they focused on the fact that the range of electric cars was sufficient for most people and that the cars were supposed to replace standard ICE vehicles.

The range of electrics was also demonstrated by setting hypermiling records during staged events, in which electrics were run at slow and constant speed over carefully selected roads using special tires.

Already in 1899, two American engineers covered 100 miles (160 km) on a single charge. In 1909, Emil Gruenfeldt of the Baker Motor Vehicle Company covered 161 miles (260 km) on a single charge in his Baker Electric Roadster. Two years later, he beat his earlier mark by travelling 202 miles (324 km) without recharging the batteries.

Data of French record runs, name a range of 191 miles (307 km) as early as 1901, set at an average speed of 17 km/h by Louis Krieger, a record that stood until 1942. In 2009, the Tesla Roadster set a new hypermiling record for electric vehicles: 311 miles or 501 km on a single charge. This result was obtained at a speed of 55 km/h.

In 1909 “Electrical World” wrote: “The average EV, as built today, has considerably more available mileage on one charge of battery than the average vehicle of ten years ago, and what is more, has a considerably greater mileage than is actually needed in the run of business or pleasure, except where a long tour is undertaken.”

It seems that 120 years ago we were already where we are today, so what has changed?

Figure 2: LowTechMagazine 2010, Link in Links and Resources below

3. The current EV market

Driven by vast global subsidies and government support programs, sales of electric vehicles reached another milestone in 2023 with 14 Mln EVs sold. Electric and hybrid cars apparently accounted for about 18% of all cars sold in 2023, up from a 14% share in 2022 and just 2% in 2018. Nearly one in five new cars sold in 2023 was electric/hybrid and although more than 90% of sales were in China, Europe, and the United States, China led the way with almost 60% of total sales with Europe at nearly 25% (IEA World Energy Investment – Link in Links and Resources below)

The total “electric” globally fleet consisted of just over 40 Mln vehicles, counting less than 30 Mln actual EVs, the others are plug-in hybrids (Figure 3: Electric and Plug-in vehicle stock), which I don’t consider an Electric Vehicle, I drive one myself from time to time and can tell you they are about optimizing fuel consumption (which is great), but not about replacing combustion engines.

Figure 3: Electric and Plug-in vehicle stock. Source: IEA Global EV Outlook, Apr 2024. Link in Links and Resources below

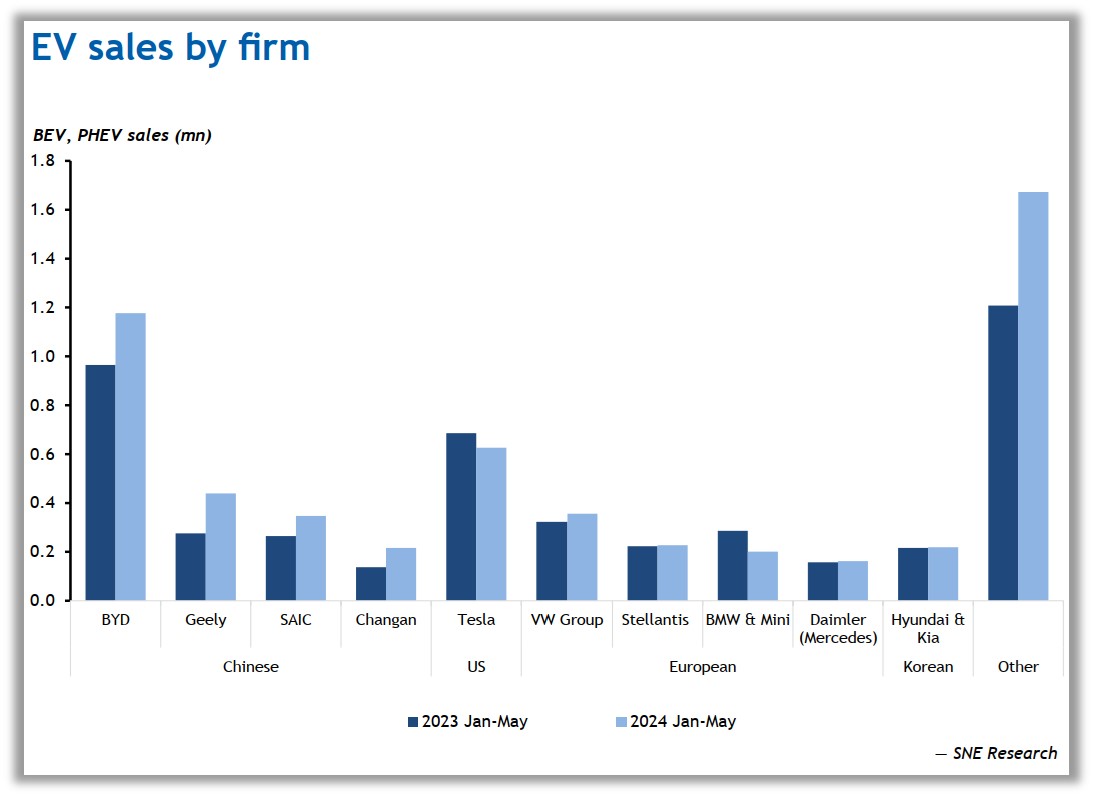

China is at the forefront of the electric vehicle (EV) market, demonstrating significant diversification. Major companies like BYD are setting new production standards, pushing traditional leaders such as Tesla into a smaller market share.

The top 15 car manufacturers collectively produce 80% of the world’s EVs. Among these, Chinese company BYD is the clear leader in sales and continues to grow (see 4: Figure EV Sales).

Meanwhile, Tesla’s share of global EV sales has declined to less than 15% in the first half of 2024, although it maintains a larger installed base. Despite this, Tesla is gradually losing market position (see Figure 5: EV Market Share) and a word on Tesla later.

Figure 4: EV sales, SNE Research

Figure 5: EV Market Share. Visual Capitalist, Mar 2024, Link in Links and Resources below

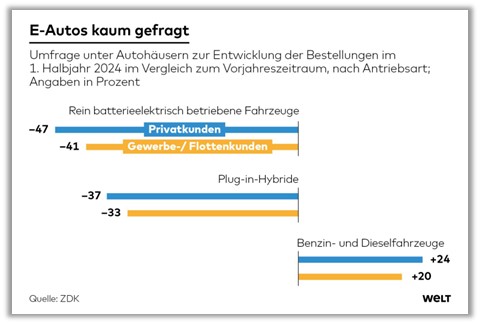

In Europe, new electric car registrations reached over 3 million in 2023, marking a substantial increase of almost 20% compared to 2022. European governments have historically offered some of the world’s most “generous incentives” funded by taxpayers for the purchase of new EVs. However, these subsidies are beginning to wind down, notably in France, where a EUR 7.000 (assume 1,1 USD per 1 EUR for simple conversion) per vehicle bonus is set to drop to EUR 4.000 in 2024 and Germany bringing its EUR 4.500 subsidy for the purchase of a new EV to an end. (IEA World Energy Investment 2024, p144-146).

Surprise, surprise, without any delay, the first “worrying” headlines started to appear:

Figure 6: Germany H1 2024 EV sales. Source: Welt – Link in Links and Resources below

Figure 7: Who buys EVs, Schernikau based on Gallup 2023

While most surveys published appear to be pro EV, the McKinsey 2024 Consumer Survey uncovered that 29% of electric vehicle owners consider to switch back to a traditional combustion engine car (Link in Links and Resources below) . This is an interesting unpopular surprise to many?

So far it remains a fact that EVs are usually bought as a 2nd, third, or even fourth car by more affluent people (Figure 7: Who buys EVs). Consider Germany or North America, who drives EVs and do they have a combustion engine car in the garage as well? Who lives in the city or who are homeowners with a charging station?

4. Car companies, EV and non-EV

What is interesting to see is how EV companies are faring out in the market. How difficult is it to build an EV manufacturer? In theory, we all can “invent” a new EV brand and start an EV company within 2-3 years with the 5 following key elements

There is even a whole website on it 😉 Launching your Electric vehicle startup – FasterCapital (Link in Links and Resources below)

Of course, there is more to it, but you get the point… the barriers to entry to build a business are much lower for an EV car than for a standard combustion engine car, which has a higher degree of mechanical complexity.

While some of us more technically minded people may love mechanical mastery, such complexity is not required for every business and often not wanted by customers. What is relevant here is the fact that the low barriers to entry for EVs basically mean business margins will also be lower on average… or even negative?

EV startup companies such as Rivian, Lordstown, Lucid, Vinfast, Polestar, Canoo, Fisker tell the stories about losing billions of dollars of investor money fast! (see the post about the article at WSJ 2024 in the references).

In addition to the low barriers to entry there are concerns about costs and of course the service that EVs provide compared to standard cars. I do not doubt and fully agree that there absolutely is a market for electric cars for instance in dense city centers for fixed routine work or the golf course (oh wait, they are already working there). What I am trying to say is that many EVs have a utility to customers that makes a lot of sense… the problem is the completely unrealistic and undesirable attempt to replace practically 1+ billion vehicles globally with EVs. Please consider the impact such a venture has on our power grids and the mining, refining, and disposal industries (see Part 2 of this series).

While the standard car industry has faced many difficult years, overall it has been quite profitable with leading manufacturers reaping billions of USD annually, with Ferrari and Porsche having the highest profit margins. Details at good car bad car, Which Automaker Was Actually The Most Profitable In 2023? (Link in Links and Resources below). We will talk about Tesla shortly. The same can unfortunately not be said for EV companies. (Links in Links and Resources below)

While in 2021 many companies announced “we will stop producing gasoline cars” (NYT Nov 2021 – Link in Links and Resources below), recently, more and more companies are back paddling.

“Lamborghini Doesn’t Think Electric Supercars Will Catch On.” Motor 1, Jun 2024.

“Porsche Drops EV Target Over Cooling Demand, China Slowdown”, Bloomberg, Jul 2024.

“Mercedes-Benz Delays Electrification Goal, Beefs up Combustion Engine Line-up”, Reuters, Feb 2024.

“Volvo, An Early Electric Car Adopter, Cuts Off Funding For Its EV Affiliate”, WSJ, Feb 2024

“BMW Boss: Oliver Zipse with doubts about European EV strategy,” Handelsblatt, Sep 2023.

“VW Will Spend Billions on Gas Engines.”, Motor 1, Jun 2024

“GM Is Investing Almost $1 Billion in New V8 Engines,” JalOpnik, Jan 2023

A word on Tesla. The company is highly profitable and one of the most valued companies globally (Market Cap beg Aug 2024 was $775 Bln USD). However, the company has been receiving large subsidies and makes a lot of money from selling its “Zero-CO2 ” allowances to other companies. This is an interesting business model and masks the real profitability of its sold EVs, or maybe better the lack of such profitability. You can read some details here

5. CO2 footprint of EVs versus combustion engines?

When comparing the environmental impact of combustion cars with EVs, usually the life-cycle CO2 emissions are compared. This is of course logically wrong, as if CO2 , a greenhouse gas with diminishing warming impact, but also the basis for all life on earth, is the only and true measure to environmental sustainability.

There is so much more to environmental “sustainability” and I covered this subject in my recent article “The Dilemma of Pricing CO2 ”. Things to consider include what I will also cover in part 2 of this series.

But even when CO2 is counted, there appears to be a lot of uncertainty, just one example is Volvo that in 2021 already said that “emissions from making EVs can be 70% higher than petrol models” (they mean CO2 of course, emphasis on “can be”).

Obviously, such a statement has a lot of assumptions on how and where the car was built and how and where the battery is charged with which electricity source.

But I can promise you that there is not one single “Zero CO2” EV running in the world today. Clearly EVs are wrongly taxed and accounted for as “Zero-CO2 ” in countries’ and companies’ “Net-Zero Pathway” plans. Using the coal-fired grids of Poland or South Africa to charge your EV, you would have to drive over 1 Mln km to come to CO2 parity… or would you ever? See Michael Sura’s article (Link in Links and Resources below) and numbers for Poland.

There are countless analyses that confirm that if the goal is to reduce CO2 emissions from passenger cars, EVs are NOT a solution.

I will not try to recreate these analyses here. But applying a more comprehensive and realistic life-cycle view and durational lifetime of batteries, I conclude that you may drive on average 150.000 to 200.000km with an EV if you are lucky? Well, have a look at some of the reports below including the mentioned sources which will give you a glimpse of the issues and how illogical it appears to assume that EVs will substantially reduce global CO2 emissions or will make a positive difference to the environment. (Links in Links and Resources below)

Let me repeat, I do believe that EVs have a role to play in the future of mobility, but this belief is not driven by CO2 efficiency.

How it is driven, I will discuss in Part 2 of this series.

6. Summary

In this Part 1 on EVs I covered the history and current market of EVs. 30 Mln fully electric vehicles on the market globally today, make up less than 3% of the global vehicle market. New electric vehicle sales are already exceeding 15%, but “EV growth bumps” are starting to appear.

Chinese manufacturers are taking over the market fast. They are growing while western auto manufacturers are stumbling. Government subsidies and support for EVs, battery and charging infrastructure amount to billions. But the sentiment in Europe and North America is changing, with subsidies slowly drying up. Germany’s slump in EV sales in the first half of 2024 is evidential of this.

EV auto manufacturers around the globe are in trouble it seems. Incumbent companies losing billions of dollars and startups burning through their cash. There are many reasons for this which we will explore in the 2nd part on EVs.

Interesting is that the life-cycle analysis of EVs and combustion vehicles is not as favorable as often portrayed. Don’t forget that everyone is literally only counting CO2 , not the true environmental footprint along the entire value chain which goes far beyond CO2 … which is a grave mistake as I pointed out here The Dilemma of Pricing CO2 ”.

Let me repeat, I am of the honest opinion that EVs have a place in the market. They are beneficial to the consumer under certain circumstances (other than accelerating “ludicrously” fast). It is up to the consumer to choose what makes sense for her or him.

I hope I piqued your interest to read the 2nd part on EVs where I will be focusing on the impact of EVs on power systems and supply chains plus exploring the future. We will also review some of those safety hazards of EVs, which are more substantial than I thought before I started researching for this article.

Links and Resources

Here are all sources and references mentioned in the article, more or less in order of appearance

{kind=link}